Between September 2025 and March 2026, Match-Prime Liquidity’s infrastructure was tested by four distinctly different market stress events – a scheduled economic release, an unscheduled exchange outage, a historic precious metals crash, and a geopolitical supply shock – each with its own cause, instrument, and mechanism of disruption.

Match-Prime’s execution data across all four tells a consistent story: tighter spreads, higher tick volumes, and deeper executable order books than comparable providers, delivered precisely during the sessions when many liquidity sources either degraded sharply or withdrew entirely.

What follows is the data from each event and an explanation of the infrastructure that produced those outcomes.

1. September 2025 NFP Release

Date: 6 September 2025 | Event: US Non-Farm Payrolls release | Instruments: EURUSD, XAUUSD

Non-Farm Payrolls is the monthly stress test every FX broker anticipates. The release window concentrates volume, widens spreads, and exposes the difference between providers that maintain genuine market depth and those that thin out when conditions intensify.

Match-Prime benchmarked its performance against three comparable Prime of Prime providers during the September release window.

EURUSD during NFP

| Provider | Match-Prime | LP 1 | LP 2 | LP 3 |

| Avg. Spread | 0.0000822 | 0.0000897 | 0.000229 | 0.001013 |

| Tick Volume | 1,300 | 1,180 | 320 | 700 |

XAUUSD during NFP

| Provider | Match-Prime | LP 1 | LP 2 | LP 3 |

| Avg. Spread | 0,125 | 0,145 | 1,1 | 0,145 |

| Tick Volume | 3,100 | 2,300 | 250 | 1,050 |

During high-impact releases, two metrics matter more than any others: spread width and tick frequency. A tight spread with sparse ticks means your larger orders face execution risk – there may be a price on the screen, but limited depth behind it.

Match-Prime delivered the tightest spreads and the highest tick volume on both instruments. One liquidity provider widened nearly 3x on EURUSD while delivering only a quarter of Match-Prime’s tick volume.

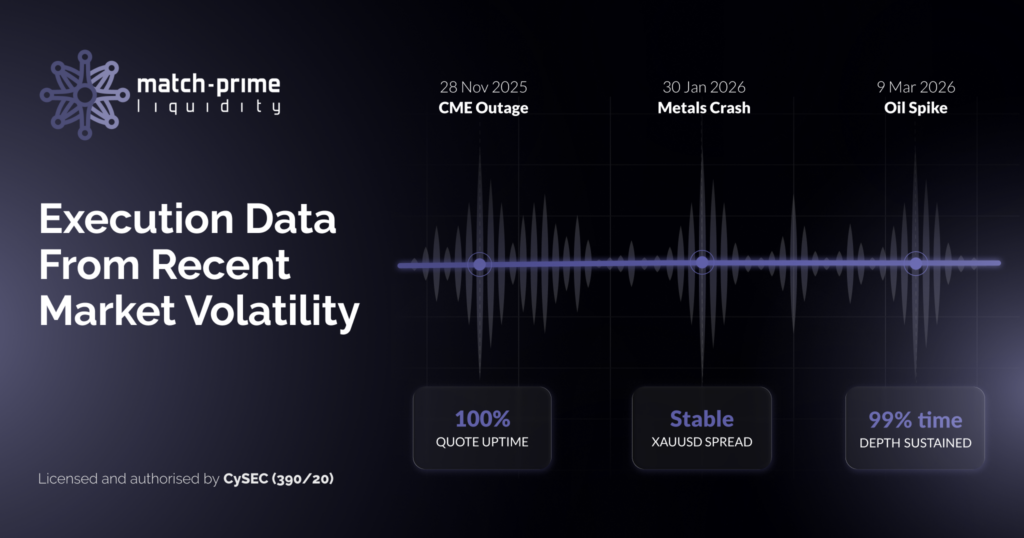

2. November 2025 CME Outage

Date: 28 November 2025 | Event: CME Group infrastructure outage | Instrument: XAUUSD

Providers can prepare for scheduled events. Exchange infrastructure failures are a different matter. On 28 November 2025, a CME Group outage disrupted gold pricing across the industry. For any provider dependent on a single pricing source, the consequences were immediate – degraded quotes or no quotes at all.

XAUUSD during CME outage

| Provider | Match-Prime | LP 1 | LP 2 | LP 3 |

| Avg. Spread | 1.0 | 2.5 | 7.5 | 4.5 |

| Tick Volume | 6,000 | 4,200 | 250 | 2,500 |

| Quotes Uptime | 100% | 85% | 45% | 92% |

One provider’s quote availability dropped to 45%, leaving brokers unable to execute for more than half of the disruption period. Match-Prime, by contrast, maintained 100% quote uptime with spreads approximately 7x tighter.

This outcome was a direct result of multi-source aggregation with automated failover. When the CME feed degraded, Match-Prime’s routing logic through Match-Trade’s Engine shifted flow to alternative pricing sources in milliseconds, without manual intervention.

3. January 2026 Precious Metals Crash

Date: 30 January 2026 | Event: Historic precious metals selloff | Instruments: XAUUSD, XAGUSD

Gold recorded its steepest single-day decline since 1983, falling nearly 10%. Silver collapsed 20–35% after reaching an all-time high the previous session. CME Group raised margin requirements mid-session, triggering widespread stop-loss cascades and a liquidity vacuum across metals markets. The combination of hawkish Fed chair nomination expectations, forced deleveraging, and crowded-trade unwinding created the kind of disorderly selloff that breaks execution quality at most providers.

XAUUSD (Gold)

| Metric | Match-Prime | Comparable LPs |

| Average Spread | 0.70 | 1.13–2.22 |

| Tick Volume | 1.35 million | Significantly lower |

XAGUSD (Silver)

| Metric | Match-Prime | Comparable LPs |

| Average Spread | 0.085 | 0.17–0.19 |

| Tick Volume | 1.17 million | Significantly lower |

| Avg. Execution Time | 16ms | — |

| Fill Ratio | 99% | — |

Match-Prime recorded the highest tick volume among all benchmarked providers on both gold and silver, reflecting continuous quote availability at a time when competing sources either reduced pricing frequency or stopped quoting entirely. On silver – a more volatile and thinner instrument – a 99% fill ratio with 16ms average execution during a 20–35% intraday collapse is an infrastructure outcome, not a coincidence.

4. March 2026 Oil Price Spike

Date: 9 March 2026 | Event: Geopolitical oil supply shock | Instrument: Brent Crude

Following weekend escalations around the Strait of Hormuz, Brent crude gapped sharply higher at Monday’s open and continued to surge intraday, with gains exceeding 30% – a move of comparable severity to the 2019 Aramco attack. US-Israeli strikes on Iranian oil infrastructure, combined with Iran’s effective closure of the Strait of Hormuz, disrupted approximately 20% of global oil supply and sent an immediate shockwave through every energy-exposed book.

Moves of this magnitude trigger a defensive reflex across the broader market. Liquidity providers typically respond by reducing market depth, widening spreads, and pulling volume from one side of the book. For a brokerage, this sudden drop in reliable liquidity turns a volatile market event into an execution crisis.

Match-Prime’s Brent Crude Performance

- Sustained depth: Match-Prime maintained its standard book depth for 99% of the period covering the gap and volatile hours that followed.

- Balanced volume: Both sides of the order book remained stable, showing only a marginal decrease in available volume.

Where competing providers typically show an immediate, structural shift – reduced depth and increased volume asymmetry – Match-Prime’s infrastructure maintained balanced, executable pricing throughout. Geopolitical price shocks are inevitable. The execution crises that often accompany them do not have to be.

The Pattern Across Four Events

Taken individually, these four events had almost nothing in common. From a scheduled data release and a technology failure, to a leveraged market crash and a geopolitical supply shock, they each involved different instruments, different volatility mechanisms, and different time horizons. The one constant across all of them was Match-Prime’s performance: spreads that remained controlled, depth that stayed available, and quotes that continued without interruption.

That consistency is not accidental. It comes from layers of infrastructure investment that compound over time.

What This Means for Brokers

For broker executives evaluating liquidity partners, these technical metrics translate into business outcomes.

Fewer client escalations. When your LP maintains stable pricing through NFP, an exchange outage, or a historic metals crash, your dealing desk is not fielding complaints about spread spikes or rejected orders.

More predictable execution costs. Spreads that remain controlled during peak volatility mean your markup calculations remain valid precisely when volume is highest – the sessions that typically account for a disproportionate share of annual revenue.

Greater operational confidence. Knowing your liquidity infrastructure has been tested and documented through actual market stress events – not simulations – materially reduces the risk.

Why Match-Prime?

The next period of acute market stress may be entirely predictable, or it may arrive without any warning at all – which is why the quality of your liquidity infrastructure matters long before conditions deteriorate.

Match-Prime is built for both: the volatility you can plan around and the disruption that arrives without warning.